Smoothing time series

Time series decomposition allows us to extract distinct components from time series data. The smoothing technique enables us to forecast the future values of time series data. In this recipe, we introduce how to use the HoltWinters function to smooth time series data.

Getting ready

Ensure you have completed the previous recipe by generating a time series object and storing it in two variables: m and m_ts.

How to do it…

Please perform the following steps to smooth time series data:

- First, use

HoltWintersto perform Winters exponential smoothing:> m.pre <- HoltWinters(m) > m.pre Holt-Winters exponential smoothing with trend and additive seasonal component. Call: HoltWinters(x = m) Smoothing parameters: alpha: 0.8223689 beta : 0.06468208 gamma: 1 Coefficients: [,1] a 1964.30088 b 32.33727 s1 -51.47814 s2 17.84420 s3 146.26704 s4 70.69912

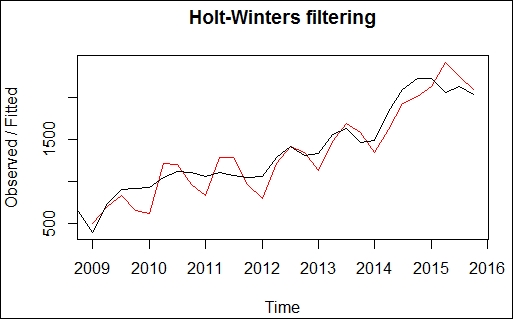

- Plot the smoothing result:

> plot(m.pre)

Figure 9: A time series plot with Winters exponential...