Execute the following steps to backtest a strategy based on the Bollinger Bands.

- Import the libraries:

import backtrader as bt

import datetime

import pandas as pd

- The template of the strategy is presented:

class BBand_Strategy(bt.Strategy):

params = (('period', 20),

('devfactor', 2.0),)

def __init__(self):

# some code

def log(self, txt):

# some code

def notify_order(self, order):

# some code

def notify_trade(self, trade):

# some code

def next_open(self):

# some code

The __init__ block is defined as:

def __init__(self):

# keep track of close price in the series

self.data_close = self.datas[0].close

self.data_open = self.datas[0].open

# keep track of pending orders/buy price/buy commission

self.order = None

self.price = None

self.comm = None

# add Bollinger Bands indicator and track the buy/sell signals

self.b_band = bt.ind.BollingerBands(self.datas[0],

period=self.p.period,

devfactor=self.p.devfactor)

self.buy_signal = bt.ind.CrossOver(self.datas[0],

self.b_band.lines.bot)

self.sell_signal = bt.ind.CrossOver(self.datas[0],

self.b_band.lines.top)

The log block is defined as:

def log(self, txt):

dt = self.datas[0].datetime.date(0).isoformat()

print(f'{dt}, {txt}')

The notify_order block is defined as:

def notify_order(self, order):

if order.status in [order.Submitted, order.Accepted]:

return

if order.status in [order.Completed]:

if order.isbuy():

self.log(

f'BUY EXECUTED --- Price: {order.executed.price:.2f}, Cost: {order.executed.value:.2f}, Commission: {order.executed.comm:.2f}'

)

self.price = order.executed.price

self.comm = order.executed.comm

else:

self.log(

f'SELL EXECUTED --- Price: {order.executed.price:.2f}, Cost: {order.executed.value:.2f}, Commission: {order.executed.comm:.2f}'

)

elif order.status in [order.Canceled, order.Margin,

order.Rejected]:

self.log('Order Failed')

self.order = None

The notify_trade block is defined as:

def notify_trade(self, trade):

if not trade.isclosed:

return

self.log(f'OPERATION RESULT --- Gross: {trade.pnl:.2f}, Net: {trade.pnlcomm:.2f}')

The next_open block is defined as:

def next_open(self):

if not self.position:

if self.buy_signal > 0:

size = int(self.broker.getcash() / self.datas[0].open)

self.log(f'BUY CREATED --- Size: {size}, Cash: {self.broker.getcash():.2f}, Open: {self.data_open[0]}, Close: {self.data_close[0]}')

self.buy(size=size)

else:

if self.sell_signal < 0:

self.log(f'SELL CREATED --- Size: {self.position.size}')

self.sell(size=self.position.size)

- Download the data:

data = bt.feeds.YahooFinanceData(

dataname='MSFT',

fromdate=datetime.datetime(2018, 1, 1),

todate=datetime.datetime(2018, 12, 31)

)

- Set up the backtest:

cerebro = bt.Cerebro(stdstats = False, cheat_on_open=True)

cerebro.addstrategy(BBand_Strategy)

cerebro.adddata(data)

cerebro.broker.setcash(10000.0)

cerebro.broker.setcommission(commission=0.001)

cerebro.addobserver(bt.observers.BuySell)

cerebro.addobserver(bt.observers.Value)

cerebro.addanalyzer(bt.analyzers.Returns, _name='returns')

cerebro.addanalyzer(bt.analyzers.TimeReturn, _name='time_return')

- Run the backtest:

print('Starting Portfolio Value: %.2f' % cerebro.broker.getvalue())

backtest_result = cerebro.run()

print('Final Portfolio Value: %.2f' % cerebro.broker.getvalue())

- Plot the results:

cerebro.plot(iplot=True, volume=False)

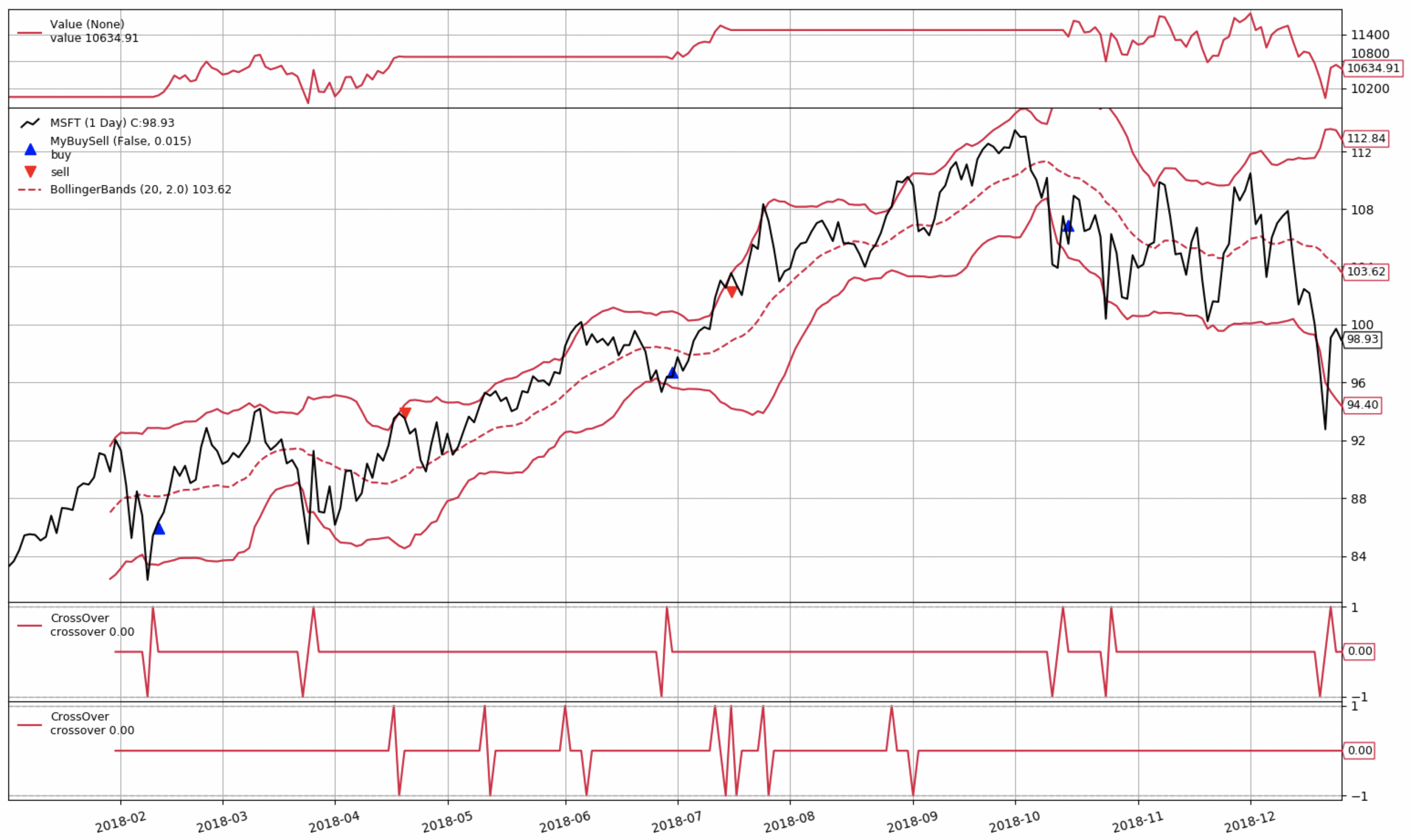

The resulting graph is presented below:

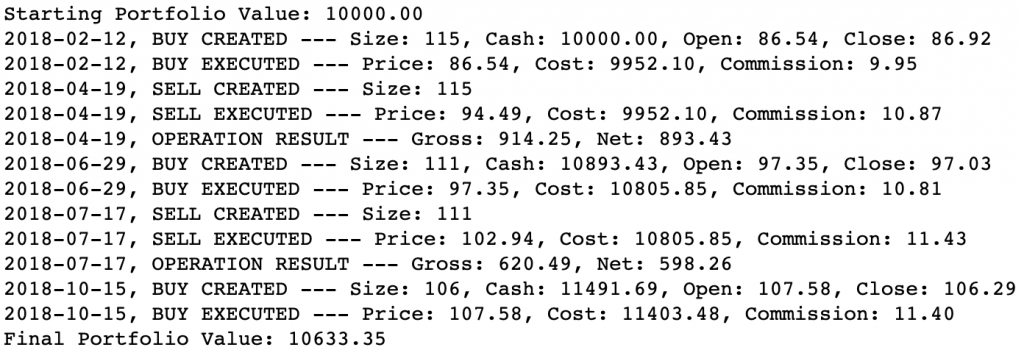

The log is presented below:

We can see that the strategy managed to make money, even after accounting for commission costs. We now turn to an inspection of the analyzers.

- Run the following code to investigate different returns metrics:

print(backtest_result[0].analyzers.returns.get_analysis())

The output of the preceding line is as follows:

OrderedDict([('rtot', 0.06155731237239935),

('ravg', 0.00024622924948959743),

('rnorm', 0.06401530037885826),

('rnorm100', 6.401530037885826)])

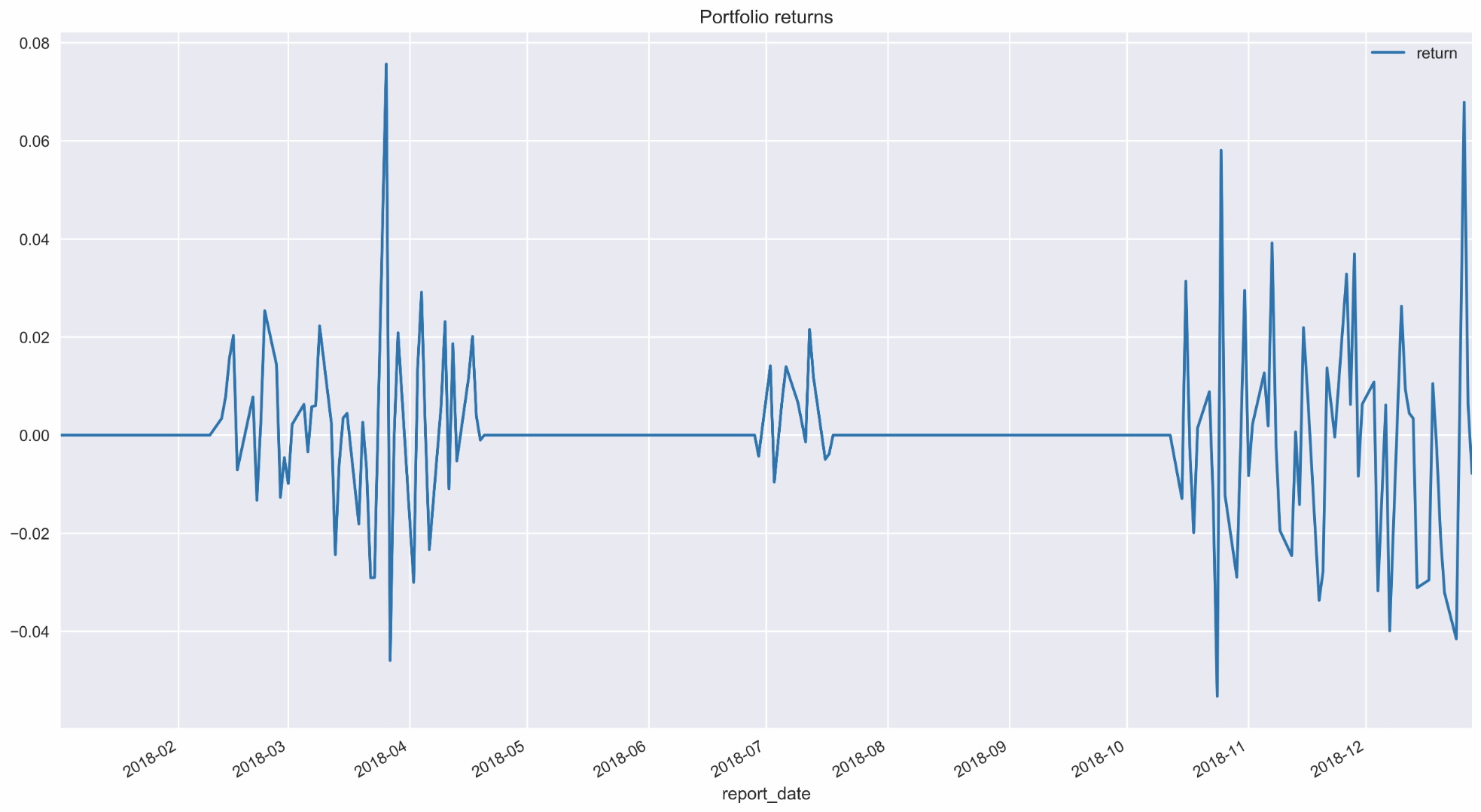

- Create a plot of daily portfolio returns:

returns_dict = backtest_result[0].analyzers.time_return.get_analysis()

returns_df = pd.DataFrame(list(returns_dict.items()),

columns = ['report_date', 'return']) \

.set_index('report_date')

returns_df.plot(title='Portfolio returns')

Running the code results in the following plot:

The flat lines represent periods when we have no open positions.