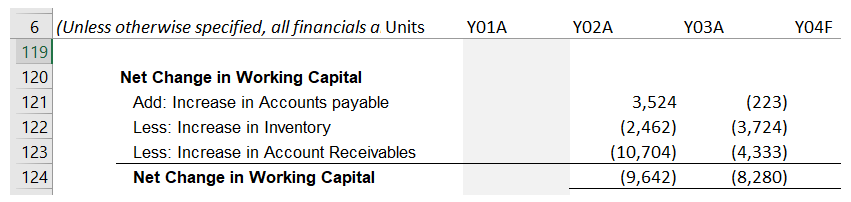

Let's look at the following screenshot on the net change in working capital:

This section converts our profit from the accrual basis into cash-based profit. In simple terms, taking our previous example, we have recorded a sale of N100,000, increasing our profit by that amount even though no cash was received. This section looks at the corresponding increase in accounts receivable of N100,000 and treats it as an outflow to be deducted before arriving at cash flow from operating activities, hence reversing the inflow recorded from the credit sale.

In summary, under this section, we add increases in working capital liabilities and subtract increases in working capital assets. An increase is manifested when we subtract the current year's figure from the previous year's, assuming that this year's figure is higher than that of the previous...