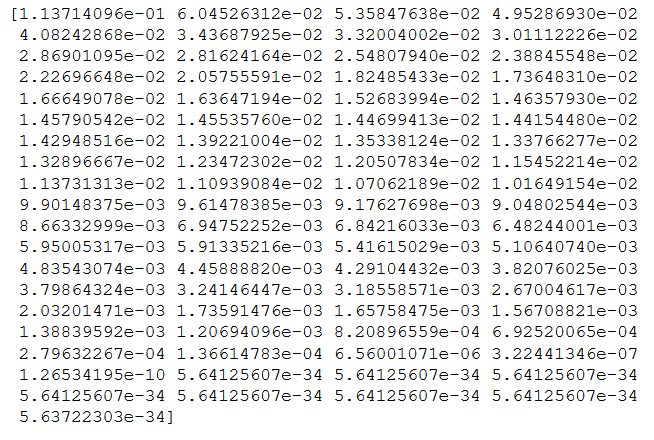

Suppose that you would like to build a predictor for an individual's expected net fiscal worth at age 45. There are a huge number of variables to be considered: IQ, current fiscal worth, marriage status, height, geographical location, health, education, career state, age, and many others you might come up with, such as number of LinkedIn connections or SAT scores.

The trouble with having so many features is several-fold. First, the amount of data, which will incur high storage costs and computational time for your algorithm. Second, with a large feature space, it is critical to have a large amount of data for the model to be accurate. That's to say, it becomes harder to distinguish the signal from the noise. For these reasons, when dealing with high-dimensional data such as this, we often employ dimensionality reduction techniques, such as PCA. More information on the topic can be found at https://en.wikipedia.org/wiki/Principal_component_analysis.

PCA allows us to take our features and return a smaller number of new features, formed from our original ones, with maximal explanatory power. In addition, since the new features are linear combinations of the old features, this allows us to anonymize our data, which is very handy when working with financial information, for example.