To make the code more readable, we first present the general outline of the class (trading strategy) and then define separate pieces in the following code blocks.

- The template of the strategy is presented below:

class SmaStrategy(bt.Strategy):

params = (('ma_period', 20), )

def __init__(self):

# some code

def log(self, txt):

# some code

def notify_order(self, order):

# some code

def notify_trade(self, trade):

# some code

def next(self):

# some code

The __init__ block is defined as:

def __init__(self):

self.data_close = self.datas[0].close

self.order = None

self.price = None

self.comm = None

self.sma = bt.ind.SMA(self.datas[0],

period=self.params.ma_period)

The log block is defined as:

def log(self, txt):

dt = self.datas[0].datetime.date(0).isoformat()

print(f'{dt}, {txt}')

The notify_order block is defined as:

def notify_order(self, order):

if order.status in [order.Submitted, order.Accepted]:

return

if order.status in [order.Completed]:

if order.isbuy():

self.log(f'BUY EXECUTED --- Price: {order.executed.price:.2f}, Cost: {order.executed.value:.2f}, Commission: {order.executed.comm:.2f}')

self.price = order.executed.price

self.comm = order.executed.comm

else:

self.log(f'SELL EXECUTED --- Price: {order.executed.price:.2f}, Cost: {order.executed.value:.2f}, Commission: {order.executed.comm:.2f}')

self.bar_executed = len(self)

elif order.status in [order.Canceled, order.Margin,

order.Rejected]:

self.log('Order Failed')

self.order = None

The notify_trade block is defined as:

def notify_trade(self, trade):

if not trade.isclosed:

return

self.log(f'OPERATION RESULT --- Gross: {trade.pnl:.2f}, Net: {trade.pnlcomm:.2f}')

The next block is defined as:

def next(self):

if self.order:

return

if not self.position:

if self.data_close[0] > self.sma[0]:

self.log(f'BUY CREATED --- Price: {self.data_close[0]:.2f}')

self.order = self.buy()

else:

if self.data_close[0] < self.sma[0]:

self.log(f'SELL CREATED --- Price: {self.data_close[0]:.2f}')

self.order = self.sell()

The code for data is the same as in the signal strategy, so it is not included here, to avoid repetition.

- Set up the backtest:

cerebro = bt.Cerebro(stdstats = False)

cerebro.adddata(data)

cerebro.broker.setcash(1000.0)

cerebro.addstrategy(SmaStrategy)

cerebro.addobserver(bt.observers.BuySell)

cerebro.addobserver(bt.observers.Value)

- Run the backtest:

print(f'Starting Portfolio Value: {cerebro.broker.getvalue():.2f}')

cerebro.run()

print(f'Final Portfolio Value: {cerebro.broker.getvalue():.2f}')

- Plot the results:

cerebro.plot(iplot=True, volume=False)

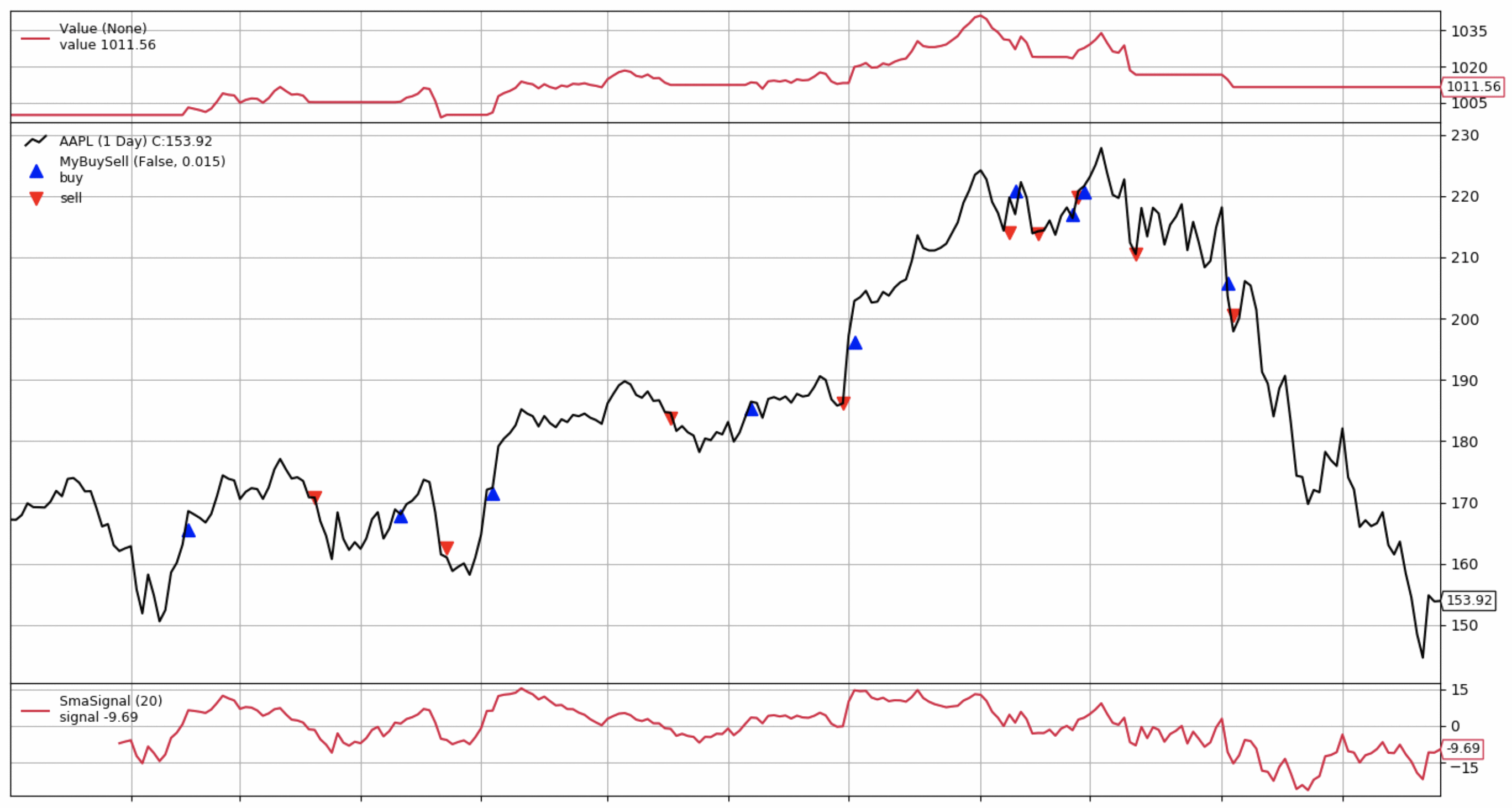

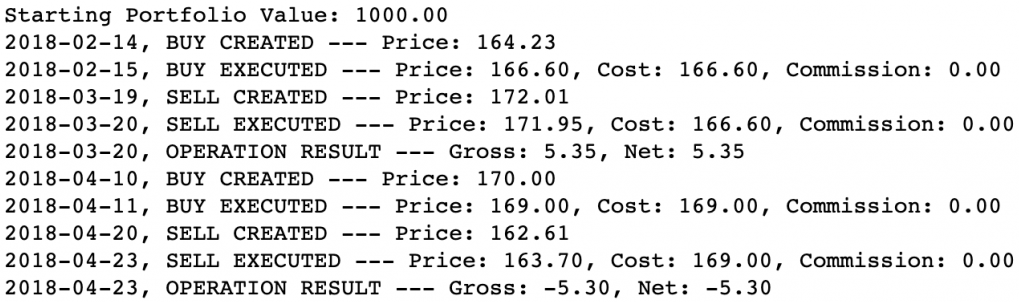

The resulting graph is presented below:

From the preceding graph, we see that the strategy managed to make $11.56 over the year. Additionally, we present a piece of the log:

The log contains information about all the created and executed trades, as well as the operation results, in case it was a sell.