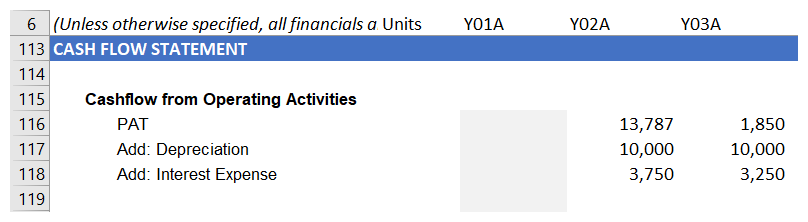

In arriving at PAT, a number of items not involving the movement of cash have been considered, which now have to be reversed in order to arrive at an accurate figure for cash flow, as shown here:

The obvious candidate for this is depreciation. The relevant cash flow occurs at the time the asset is purchased. However, we don't charge the total cost to the profit and loss account all at once; the correct accounting treatment is to allocate the original cost over the useful life of the asset.

This periodic allocation of cost is called depreciation and clearly does not involve the movement of cash. Since it has been deducted as an expense in arriving at our profit, we need to add it back to the PAT, as shown in the preceding screenshot. We also add back interest charged to PAT. Although this is cash flow, it is the cost of debt finance...